Although global equities ended February broadly flat, the first two months of the year have been anything but dull with events in China, the Middle East, Europe and the US competing for headlines. Many stock markets closed 2024 at all-time highs and against a backdrop of rising conflict and political change, the ride for investors in 2025 was always likely to be bumpy, explains Knut Gezelius, Lead Portfolio Manager of SKAGEN Global: “Equity markets have produced several surprises this year, but they were always likely to make some wild gyrations during Trump’s second presidency and particularly at the outset. It is important to keep emotions in check and focus on the road ahead, rather than get distracted by the political posturing that will likely continue to dominate the news agenda in the medium-term.”

European resurgence

The biggest surprise has perhaps been the strong performance of European equities. The Stoxx 600 index closed February up 9%, delivering a new all-time high and its best start to a year since 1987. Also unexpected has been the sluggish performance of US equities – the S&P 500 index has 1% higher year-to-date and lags the European return by its largest margin in almost a decade.

This follows a dramatic mood swing from the end of last year. February’s Bank of America’s global fund manager survey showed investor positions in Eurozone equities rising to a net 12% overweight versus a net 25% underweight in December. US equity exposure has meanwhile fallen to a net 17% overweight from its 36% peak at year-end. According to EPFR, the third week of February saw the largest inflows into European equity funds since early 2022.

Several factors are driving Europe’s revival. There has been relief that Donald Trump decided against an immediate introduction of tariffs on EU imports, despite his pre-election threats and perceptions that European companies posed a significant threat to his ‘America First’ policies. This has boosted economic growth prospects in Europe and prompted analysts to raise earnings estimates by 0.6% since the start of year, versus a 1.0% downgrade for US companies according to Bloomberg.

“We don’t try to predict who will win the tariff game,” explains Gezelius, “Instead we focus on constructing a portfolio to navigate a wide variety of macro scenarios. The current global situation has only strengthened our view that the best investments are well-managed businesses with strong balance sheets that that can withstand unexpected volatility.”

SKAGEN Global added several such companies during the second half of last year with sizable positions especially in the Italian mid-cap luxury company Brunello Cucinelli and the dominant global reinsurer Munich Re headquartered in Germany. “Each was introduced to the portfolio based on our bottom-up analysis that showed a combination of a resilient business model, competitive edge and undervalued share price,” adds Gezelius, “We also sold some European holdings – our goal is always to create a balanced portfolio, but we look at many factors and business drivers beyond where a company is listed.” SKAGEN Global closed February around 4.8% ahead of the MSCI AC World Index year-to-date.

Peace dividend

European equities have been given their biggest boost by the prospect of peace in Ukraine, with the region expected to benefit from falling risk premiums and energy prices as well as higher economic output. The UN estimates the Ukrainian rebuild cost to be $486bn over the next decade – potentially a drag on national finances but a huge opportunity for some companies. The European Monetary Union (EMU) Construction Materials Index is up 22% this year, for example, while Industrial Conglomerates are 17% higher[1].

The short-term outlook is blurred by the positional shifting of the US and Europe in negotiating a ceasefire, particularly regarding their post-war support for Ukraine. Talks involving Trump, Zelensky, Putin and other European leaders are ongoing but what seems certain is that Europe will have to increase its long-term defence spending, probably at the expense of health and social care or overseas aid as seen in the UK. This has pushed EMU Aerospace & Defence stocks 20% higher in 2025.

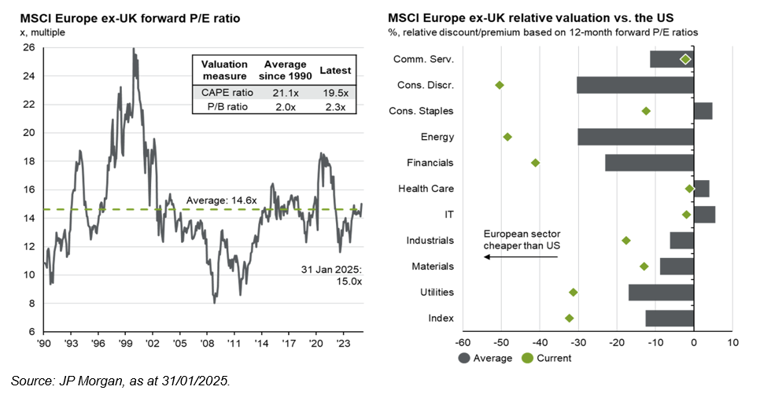

Attractive European valuations have been another draw for investors. Although stocks are only slightly cheaper now than they were when Russia invaded Ukraine in February 2022 and marginally above long-term averages, they remain around a third cheaper than US equities. Most European sectors have historically traded at a discount to their American counterparts but currently the gap in all sectors except Communication Services is wider than historic averages.

American exceptionalism

Following its strong start, the Euro Stoxx is now expected to be the top performing index this year according to nearly a quarter (22%) of respondents to Bank of America’s February survey, followed by Nasdaq (18%). A European victory in 2025 would still make little impression on the longer-term dominance of US equities with the S&P 500 total return more than double that of the Euro Stoxx 600 since 2012 when the markets began to decouple.

Nor is it likely to threaten the notion of American exceptionalism. According to the World Bank, eurozone economies were 15% bigger than the US in 1990 but are now 25% smaller, and with GDP per head in the EU currently 25% lower than America, the gap is only likely to get wider. This has translated into stock market dominance – the total value of US stocks is around four times larger than all of Europe’s stock exchanges combined (ten years ago it was less than twice the size).

“Any narrative around the demise of the US is premature. We currently have around 60% of our portfolio invested in US companies – many of these are global businesses with large international revenues, such as Alphabet, Mastercard and JP Morgan,” Gezelius argues, “While certain segments look expensive, the valuation of the US market as a whole also does not strike us as overly stretched given where US interest rate levels are today.”

A back-of-the-envelope calculation using the US 10-year generic government bond yield of 4.25% and the 24x LTM P/E of the S&P 500 indicates that the index is currently trading within 2% of its estimated fair value and is actually 6% undervalued using the forward P/E of 22x. “Other methodologies may yield different results, but we think this simple approach is a good first-degree approximation,” concludes Gezelius, “The US market still offers ample opportunity for bottom-up stock-pickers. You can still find many world-leading companies across different sectors without paying top dollar.”

[1] Source: MSCI. MSCI indices in local currency.